Hyderabad Real Estate: Deliberate recalibration of supply in CY25 augers well for structural health of residential market

In a nutshell

1. Robust economy (IT and pharma), investor-friendly government policies, superior infra, better quality of life and a steady influx of skilled talent have driven real estate growth.

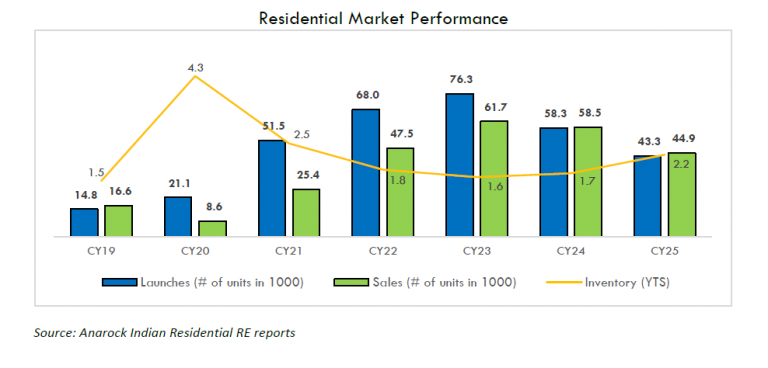

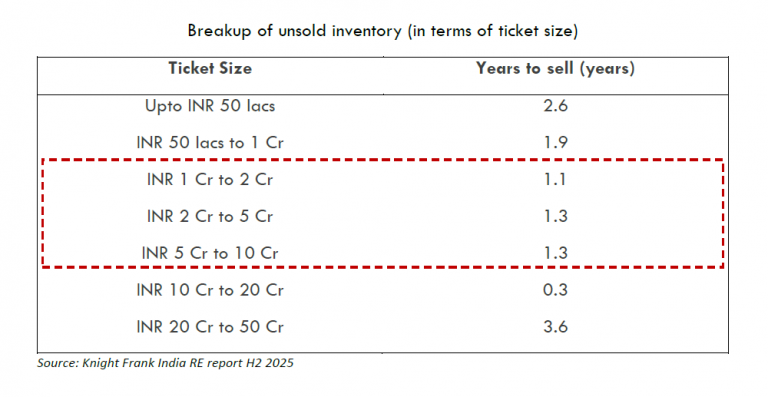

2. Residential market remains structurally healthy despite recent sales moderation, with deliberate recalibration of supply.

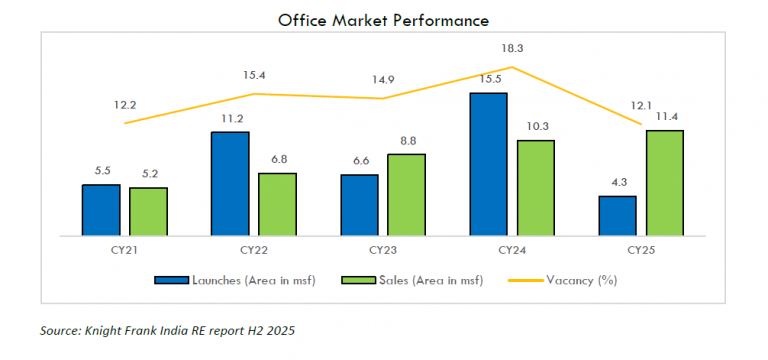

3. Office market continues to be resilient with strong leasing and improving vacancy.

4. West Hyderabad will likely further strengthen its status as premium commercial and residential district, driven by high-value land economics and Grade-A office.