India Residential Real Estate: 2014 vs 2026 – Healthier Slowdown

In a nutshell

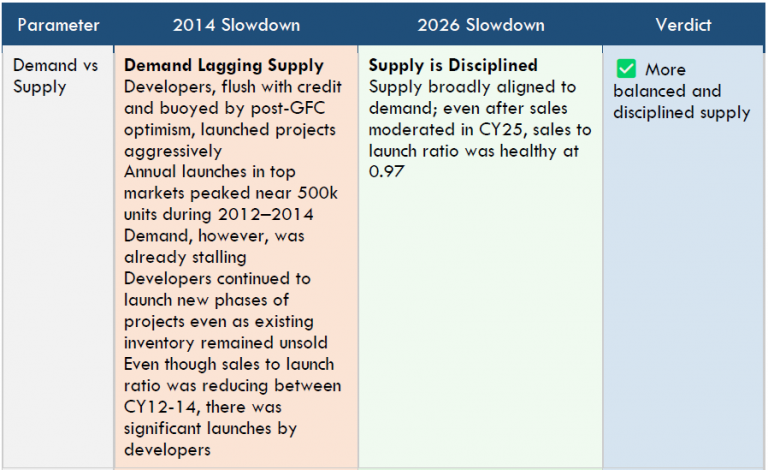

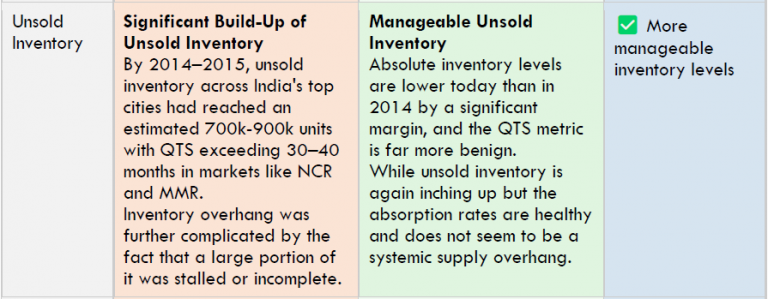

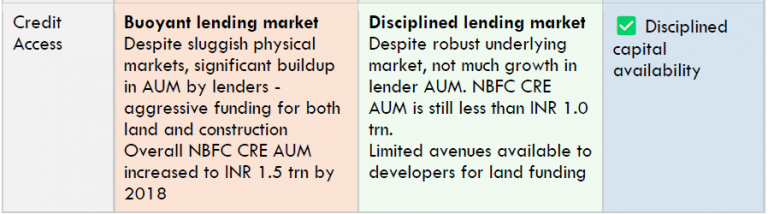

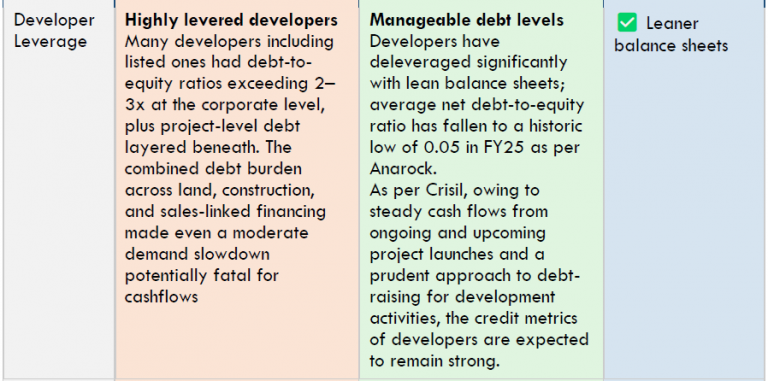

1. Current moderation in residential sales after a strong upcycle seems a far healthier pause than the 2013–2014 downturn

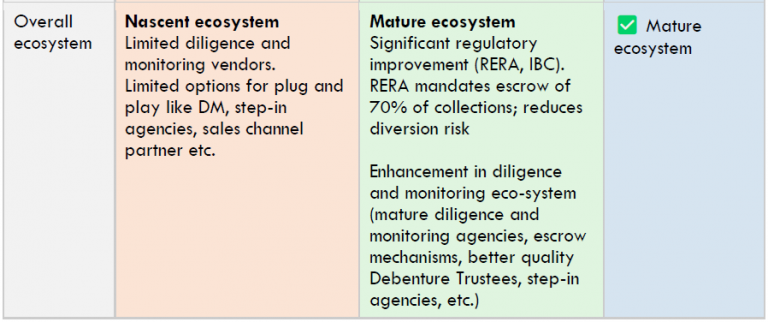

2. In the current cycle- supply from developers is more disciplined, inventory levels seems more manageable, lending market is more balanced, developer balance sheet appears less frothy and there is a mature ecosystem with more regulatory teeth.